US Beneficial Owners Roundtable 2023: Current Market Drivers and Trends

Current Market Drivers and Trends

During March 2023, Global Investor/ISF held the annual US Beneficial Owners’ Roundtable in New York with the help of EquiLend as the lead sponsor. The roundtable was moderated by Global Investor’s Managing Director Amelie Labbe-Thomson who was joined by an esteemed group of speakers to discuss recent trends, developments and challenges in the securities finance space.

A portion of the 2023 US Beneficial Owners Roundtable is available in the video above. See below for a transcript of the highlights.

Amélie Labbé, Managing Director, Global Investor Group: The global securities finance industry has generated an increasing amount of revenue for lenders since 2020, with the Americas region specifically spearheading that growth in multiple areas. We are gathered here to analyse the situation and see how recent events and potential future developments will impact this situation, which brings me to my first point today looking at current market drivers and challenges. I would like to hand over to Nancy Allen from EquiLend to take us through some key metrics to set the scene for our discussion today.

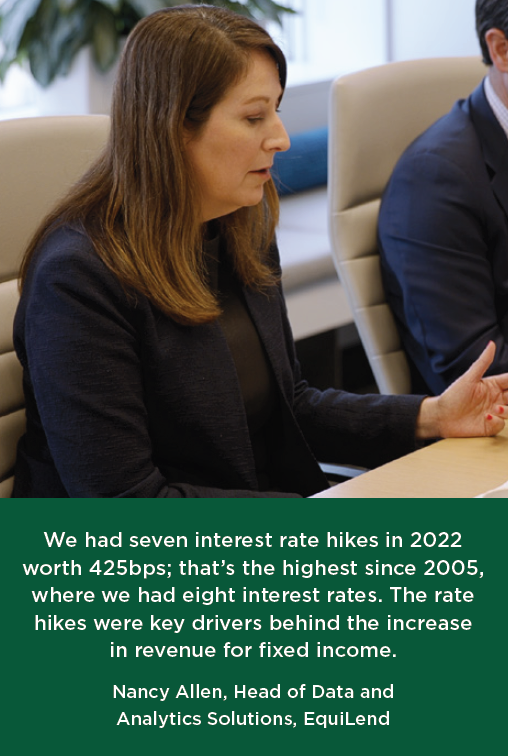

Nancy Allen, Head of Data and Analytics Solutions, EquiLend: I have a high-level overview here to set the scene for our discussion today. Looking at revenue in 2022, we were up 7% over 2021, with lender to

When you look at that 7% increase, global equities increased by 2%. Overall, global fixed income was up 25% and we’ll talk a little bit about the drivers behind that significant increase in fixed income. Looking regionally, the Americas was up 10%. Equities were up 7% in the Americas and fixed income up 19%. In EMEA, we were up 6% with equities and fixed income up 22%. In Asia, primarily dominated by equities, we were down 2%.

Jumping into a couple of highlights into some drivers of revenue. We had seven interest rate hikes in 2022 worth 425bps; that’s the highest since 2005, where we had eight interest rates. The rate hikes were key drivers behind the increase in revenue for fixed income.

What we have here is the revenue by quarter and overlaying the revenue we have the average basis points. You can definitely see an increase in the average fee going from Q1 of 2020 - of 31 basis points - up to a high of 39 in Q3. So far in Q1 2023, we’re coming in at about $2.2 billion and that’s up until March 17th.

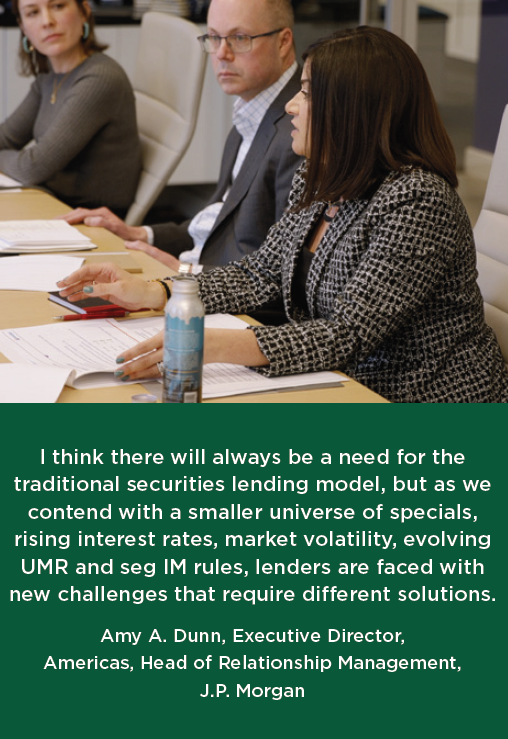

Amy Dunn, Executive Director, Americas Head of Relationship Management, J.P. Morgan: In terms of borrower behaviour, counter-parties have become acutely focused on RWA and actively targeting RWA friendly client types which are associated with the lowest capital requirements. This has led to providers smart bucketing whereby client types are grouped by their risk weighting which will dictate trade flow. For example, sovereigns and central banks are associated with the lowest RWA and highest demand whereas pensions, insurance companies and ‘40 Act Funds are associated with the highest RWA and lowest demand. This will clearly have an impact on performance based on what bucket a lender falls into.

Francesco Squillacioti, Senior Managing Director, Global Head of Client Management, State Street: I think

As Nancy points out, it was still a pretty good year. I think our performance echoed a lot of what she presented earlier. The other part is that lender participation has grown, as well. When we think about going forward and bringing new clients onto the program, we’re just trying to make sure that the types of assets that we’re bringing on are as accretive as they can be to the program as we look at what clients are looking to enrol.

Amélie Labbé: Amy, I’m just going to ask you to share what your thoughts are on what the drivers are going to be that will impact lender and borrower behaviour in the near future, but also if you can give a bit of a flavour as well on types of collateral that we’re going to be looking at as well.

Amy Dunn: On the back of Francesco’s point, I would agree that client interaction is key. As it relates to the impact of RWA or any headwind facing our industry, in order to remain relevant and competitive, strong consideration of program changes that allow for greater flexibility will be beneficial. We have a limited number of levers at our disposal but the more levers approved, the better positioned a lender is to capture the next revenue opportunity. Common considerations are: collateral flexibility, counter-party or market expansion, conducting a cost/benefit analysis ahead of recalling for proxy, increased participation in trade opportunities and review of cash collateral guidelines.

Cherie Jefferies, Director of Fixed Income Trading, State Board of Administration of Florida: When it comes to borrowers, we depend on our securities lenders to evaluate the borrowers that we use. When we look at the alternative for different collateral between the regulation and the tax harmonisation that’s transpired over the past several years, for us, that’s always evolving. We’re always looking at different types of collateral. Currently we’re looking at adding some non-cash collateral availability to our program.

We’re in the process of doing that now, so that has not been finalised, but we always are looking to keep our program abreast of the changing regulations and environment.

Brooke Gillman, Global Head of Client Relationship Management, eSeclending: I think when you talk about flexibility around guidelines, what is starting to transpire now in the industry is not just the things that Cherie and Amy and Cesco were speaking about in terms of collateral types and different sort of transaction components to what the economics are of the trade but it’s also about structural flexibility. I think that will be an ongoing theme and so there are a lot of new ways that people are approaching what are the same types of and results in terms of exposure on transactions but done through either a different legal structure or a different mechanism. We have spent time as agent around this table educating the client beneficial owner community on what they can be comfortable with on collateral and things like that.

The next five, ten years will be much more around structural differences of trade types. So whether that may be pledge models or similar models in that sense, central counter-parties, agency prime on indemnified programs, there are lots of new structural differences I think that will come into play across the marketplace in order to keep up with the needs that are being driven by these regulatory capital constraints.

Amy Dunn: I would agree. There is an increased focus on identifying ways to leverage the existing pipes

For example, lenders that employ leverage or derivative strategies may be facing new requirements that have forced organisations to think more broadly about how they approach collateral and manage liquidity. Those lenders are not only thinking about these products individually but also how they can be interconnected to optimise overall returns.

Some clients are also exploring alternative ways of utilising cash collateral. We have worked with certain clients to focus on optimisation and consider opportunities such as leveraging cash collateral raised through a securities lending transaction to finance their needs in a more cost effective way.

Found this useful?

Take a complimentary trial of the FOW Marketing Intelligence Platform – the comprehensive source of news and analysis across the buy- and sell- side.

Gain access to:

- A single source of in-depth news, insight and analysis across Asset Management, Securities Finance, Custody, Fund Services and Derivatives

- Our interactive database, optimized to enable you to summarise data and build graphs outlining market activity

- Exclusive whitepapers, supplements and industry analysis curated and published by Futures & Options World

- Breaking news, daily and weekly alerts on the markets most relevant to you